Asset Allocation guide: U.S. vs. international equity

In our ongoing series looking at asset allocation issues, we've already covered some essentials, namely, how to analyze your ability, willingness and need to take risk -- and what do when one or more of those factors conflict. Figuring out where you fit along the risk spectrum will help you figure how much of your portfolio to put into stocks.

Now, we'll start looking at some next steps. Once you've determined the appropriate percentage of stocks to hold, you'll have to to determine the appropriate mix between domestic and international stocks. (You'll also have to tackle how much to allocate to value vs. growth stocks, small-cap vs. large-cap and how much to put into real estate -- all topics we'll cover in follow-up articles.)

Investing in international stocks, while delivering expected returns similar to domestic stocks, provides the benefit of diversifying the economic and political risks of domestic investing. During long periods, U.S. stocks have performed relatively poorly compared to international stocks. The reverse has also been true.

But over the long term, returns have been similar. Thus, the gains from international diversification come from the relatively low correlation among international securities. This is especially important for those employed in the U.S. because it's likely their labor capital is highly correlated with domestic risks.

The logic of diversifying economic and political risks is why investors should consider allocating at least 30 percent, and as much as 50 percent, of their equity holdings to international equities. While the U.S now represents less than 50 percent of the global market capitalization of all stocks, at least some "home country bias" is warranted because investing in international stocks is typically a bit more costly, and it can be somewhat less tax efficient. That's why I suggest up to a 50 percent allocation (my preferred recommendation).

To obtain the greatest diversification benefit, exposure to international equities should be unhedged -- hedging the currency risk increases the correlation of returns to U.S. equities.

Reasons to increase international equity exposure

Reduced risk. The historical evidence suggests that raising the international allocation to at least 40 percent reduces portfolio risk (volatility). However, for many people, increasing the international equity exposure above 50 percent of the total equity portfolio doesn't make sense because of tracking error concerns and from a risk-return perspective. Both are addressed in the discussion below.

Investor has non-U.S. dollar expenses. An investor may live part of the year overseas, or frequently travel overseas. Such an investor should consider tailoring the portfolio to gain specific exposure to the currency in which expenses are incurred. This could also be accomplished by making fixed-income investments in the local currency.

Reasons to decrease international equity exposure

Tracking error. This is defined as underperformance versus a benchmark. Some investors may not be able to stomach the tracking error associated with a portfolio with 40 percent of its equity invested overseas.

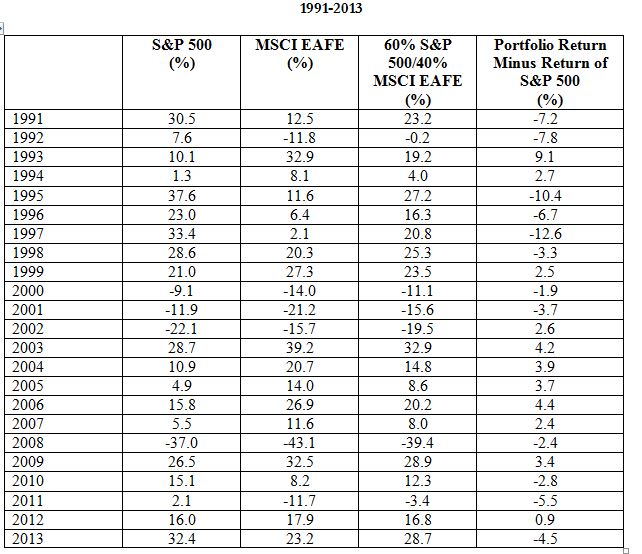

The table below illustrates tracking error risk by comparing the performance from 1991 through 2013 of a portfolio with a 100 percent allocation to U.S. stocks (S&P 500 Index) to the performance of a portfolio with a 60 percent allocation to U.S. stocks and 40 percent allocation to international stocks (MSCI EAFE Index).

While investors are pleased when there's positive tracking error (2002-07), many cannot tolerate underperforming their peers by significant margins when the tracking error turns negative, as it did from 1995 through 1998 and during four of the last six years. Unless investors can tolerate negative tracking error and rebalance when appropriate, an international allocation will not be of much value.

Costs matter

While international assets provide an important diversification benefit, international investing is more expensive because of higher trading costs and higher fund expenses, and it can be somewhat less tax efficient due to issues related to the foreign tax credit. Thus, allocating more than 50 percent to international equity may not be optimal from a risk-return perspective. An exception might be an investor whose labor capital risk is substantial. Tilting heavily toward international equity can diversify that risk.

How much to allocate to emerging markets?

Emerging markets comprise those nations whose economies are considered developing or emerging from underdevelopment. They include almost all of Africa, Eastern Europe, Latin America, Russia, the Middle East and much of Asia, excluding Japan, Hong Kong and Singapore. Many investors shy away from emerging markets, viewing them as either highly risky investments or pure speculations.

However, even though emerging markets are risky shouldn't preclude investors from allocating some portion of their portfolio to them. Modern Portfolio Theory tells us sometimes we can add risky assets and actually reduce the risk of the overall portfolio. The reason is the diversification benefit.

Here's another reason to consider investing in emerging markets: because they're a risky asset class, an efficient market will appropriately price that risk. The result is higher expected returns. Historical evidence shows that emerging market equities have high returns with high volatility. They also have low correlations to both domestic and international equities. And the evidence shows that including a small amount of emerging markets equity in a portfolio increases that portfolio's return while leaving volatility roughly the same.

Since emerging markets make up approximately 25 percent of the non-U.S. global market capitalization, I suggest that emerging markets also make up 25 percent of your total international allocation.

Reasons to increase emerging markets equity exposure

Increased expected return. The primary reason to increase one's allocation to emerging markets is to increase the portfolio's expected return. Investors who need to increase their expected return to meet their financial goals can use an allocation to emerging markets to help meet this objective.

Reasons to decrease emerging markets equity exposure

Tracking error. Emerging markets equity has a relatively low correlation with both the overall U.S. markets and international developed markets. Therefore, emerging markets' returns may be below their average when the U.S and/or other developed markets are producing above-average returns. Some investors may not be able to tolerate this tracking error. Also, the correlation of emerging markets equity could be high enough in some periods that inclusion of a large allocation to emerging markets could actually increase the overall portfolio's volatility to an unacceptable level.

The correlation of emerging markets to other equity asset classes typically rises during periods of financial turmoil. Thus, when the low correlation is most needed, the correlation is likely to increase. Investors who are either highly sensitive to tracking error risk or highly risk averse should consider limiting their exposure to emerging markets.

Having decided on the domestic vs. international allocations, our next step will be to decide how much we should allocate to value and growth stocks.

Editor's Notes: Some material for this article was adapted from the author's book, "The Only Guide You'll Ever Need to the Right Financial Plan."

You can try out CBS MoneyWatch's new online asset allocation calculator.