How will Comey affair affect stocks and the economy?

Investors are on edge after the tumult over former FBI Director James Comey's claims regarding President Donald Trump sent stocks spiraling to their biggest loss in eight months. The big question for financial markets: How bad could things get?

Some forecasters think that, in the short term at least, the worst could be a "correction," where the market falls by 5 to 10 percent. More optimistic analysts expect only a stretch of discomfort before Wall Street stages a recovery.

Although that may seem unduly sanguine given the swirling controversy in Washington over the circumstances surrounding Mr. Trump's firing of Comey, that view is based on the present trajectory of the U.S. economy, rather than political speculation. Growth this year, though hardly robust, is expected to be solid. A healthy labor market and rising corporate profits, which the U.S. is enjoying currently, tend to energize the market, which functions as a barometer of where the economy appears to be heading.

On Wednesday, on the Comey news, the Standard & Poor's 500 and the Dow Jones industrial average both slipped 1.8 percent and the Nasdaq Composite was off 2.6 percent. Overseas exchanges fell, although the losses were mild. Refuge assets like bonds and gold rose.

This marked a sharp reversal of the U.S. stock market's upward drift in recent weeks. To be sure, that rise has slowed since late April, when the House on its second try narrowly passed a revamping of Obamacare. Then came Comey's firing last week. And next was the surfacing of his memo this week that alleged the president wanted Comey to squelch the bureau's investigation of White House national security chief Michael Flynn's ties to Russia. Not helping was a news story that Mr. Trump had spilled U.S. secrets to visiting Russian diplomats, which the White House denied.

Certainly, if Mr. Trump ended up getting impeached, share prices would suffer. But tracing the market during BIll Clinton's impeachment drama two decades ago shows how easily investors can shake off bad political news when the economy is in good shape, as it is today.

For those reasons, Sam Stovall, chief investment strategist at the CFRA research firm, believes the market damage will be contained. As he wrote in a research note: "This time around, while the current crisis may trigger a correction, we do not think it will lead to recession and therefore will not result in a new bear market."

To Brad McMillan, chief investment officer for Commonwealth Financial Network, the fireworks in Washington amount to just "noise" that thus far has little relation to what's happening on Wall Street and in the broader economy. "Looking at the big picture," he argued, "to get a bigger and sustained drawdown, we need things we don't have: a recession, spiking interest rates or spiking oil prices."

Here's an assessment of the Comey fallout:

The stock market. Should Mr. Trump be impeached by the House and tried by the Senate, stocks likely would persevere, as CFRA's Stovall contends. The proviso is that the economy remain on course. That was the case during Clinton's travail over lying about his sexual dalliance with intern Monica Lewinsky. It helped that this was in the middle of the dot-com surge. While the market initially faltered as the scandal grew, stocks ended up ahead. From January 1998, when the mess came to light, to his acquittal in the Senate in February 1999, the S&P 500 rose 10.3 percent.

The Comey slide has had a special grease: When the market is expensive, as it is now, "it is much more susceptible" to a dip, noted Brent Schutte, chief investment strategist at Northwestern Mutual Wealth Management. The S&P 500's price/earnings ratio, a measure of market affordability, sits just under 24. Historically, the index's P/E averages about 15. So a correction might bring the metric back into line, or at least put it closer.

Since the election, the market has shot higher, partly on excitement over Mr. Trump's plans to stimulate the slow growing economy -- it's grown at around 2 percent annually for the last several years. But Paul Hickey, co-founder of Bespoke Investment Group, noted on CNBC on Wednesday that many overseas bourses have done even better, and they are not beneficiaries of the Trump tax or pubic works plans. This year, stocks in France, Germany, Brazil and others have climbed twice as much as the S&P 500.

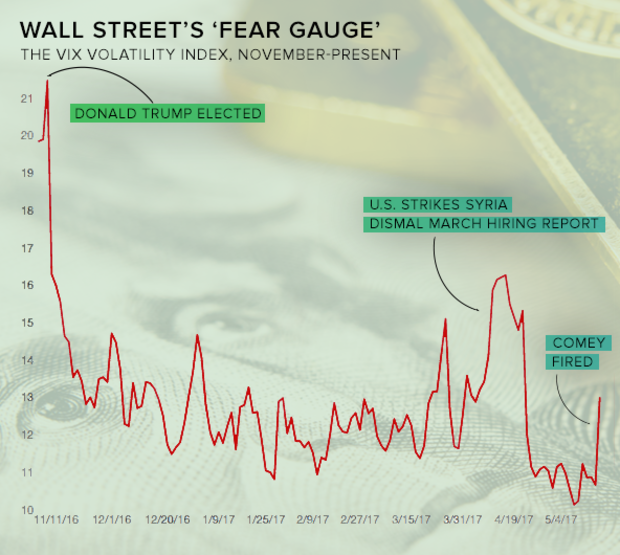

One marker of investor angst is a boost in the so-called fear index, the VIX, On Wednesday, it jumped up to 15, from a low point of around 10. When the Chicago Board Options Exchange Volatility Index, as it is formally known, reaches 20, that signals a crossover from the jitters to outright fright.

The last times that the VIX topped 20 recently were last June following Brexit, the United Kingdom's vote to leave the European Union, and right before the November presidential election. Its highest level over the past 10 years was in September 2008, the onset of the financial crisis, when it touched 60.

When storm clouds gather, some stock investors exit growth shares for the relative safety of more defensive sectors. On Wednesday, cyclical stocks in the S&P 500 like financial services (down 3.1 percent) and technology (slipping 2.7 percent) got harmed the worst. But defensive plays, notably real estate (up 0.6 percent) and utilities (ahead 0.2 percent), improved a bit. Apple (AAPL) and Facebook (FB), which had been market leaders, got slammed especially. "This is what happens in a short-term selloff," said Michael Arone, chief investment strategist at State Street Global Advisors.

The economy. Corporate earnings are doing indisputably well. For the first quarter, they were ahead about 13 percent in the U.S., according to FactSet researchers. And forecasts are for continued double-digit hikes for the balance of the year. At the same time, European companies are on track to show a 23 percent growth for the first quarter, which helps American multinationals. "We have never had a recession amid rising earnings," said State Street's Arone.

Economic indicators have been encouraging, although mixed. Industrial production in April was solid, and showed manufacturers are expecting good demand. Meanwhile, the Institute of Supply Management's non-manufacturing index showed an 88th sequential month of expansion. On the other hand, last month's auto sales shrank, indicaling a reversal of Detroit's boom. Credit delinquencies are up.

Still, said Northwestern's Schuette, "because the fundamentals are in a good place, we are talking about the pace of growth, not whether there will be a recession."

The Trump legislative agenda. When Mr. Trump showed the difficulty of passing a revamp of the health law, despite GOP majorities on Capitol Hill, many on Wall Street realized that enacting a tax reduction and a huge infrastructure buildout would take a while. Taxes and infrastructure are what excited investors in the first place, but now the economy's resilience is what seems to be animating them more.

If Trump becomes politically toxic, his economic agenda is almost certainly stalled, and quite possibly dead on arrival. With the congressional midterm elections next year, he has until roughly mid-2018 to implement his agenda on health care, taxes, infrastructure and deregulation -- a daunting set of policy objectives.

Meanwhile, the market has come to understand that the president's economic stimulus plans will be delayed or curtailed, and "Congress' agenda just went from 'busy' to 'we're booked out through the summer,'" said Gregory Daco of Oxford Economics. If Mr. Trump's stimulus plans fall through, Oxford forecasts 2018 economic growth of 2.1 percent instead of 2.7 percent.